SPOTLIGHT ON THE FED’S RISING DEBT & ITS DILEMMA

4 September 2023

The Fed Faces a Dilemma…

The Fed looks at the core PCE (Personal Consumption Expenditures Price Index, Excluding Food and Energy). In August 2023, the core PCE was 4.3%, still far from the 2% target.

You may wonder about the Fed’s commitment to its 2% inflation target. Why? To do so means a fast-rising debt for the Fed.

6X jump in the Fed’s Interest Expense…

Recently, the Fed announced a whopping USD 29.7 billion operating loss for 2Q23. This was mainly due its interest expense rocketing over 6X from the previous year to USD 11.8 billion.

Root problem is the Fed’s asset/liability mismatch…

The Fed’s problem is that it earns fixed interest on its assets while interest expense on its liabilities is variable – a classic asset/liability mismatch.

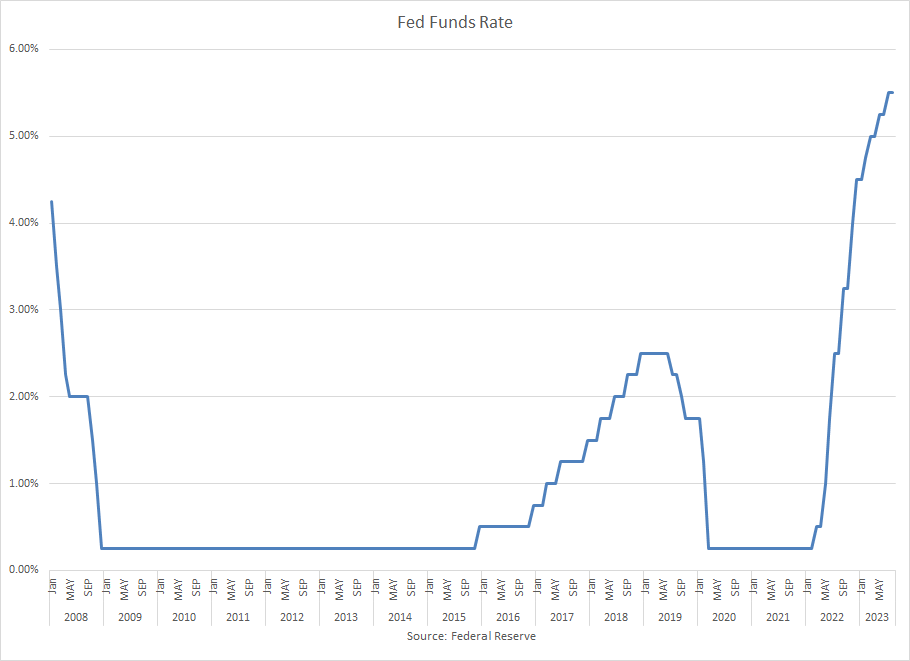

The Fed faces an escalating debt burden fire as it raises interest rates to douse inflation. Since the Fed began tightening in March 2022, it has raised the Fed Funds rate 10 times, from 0.25% to 5.5%.

Source: Federal Reserve

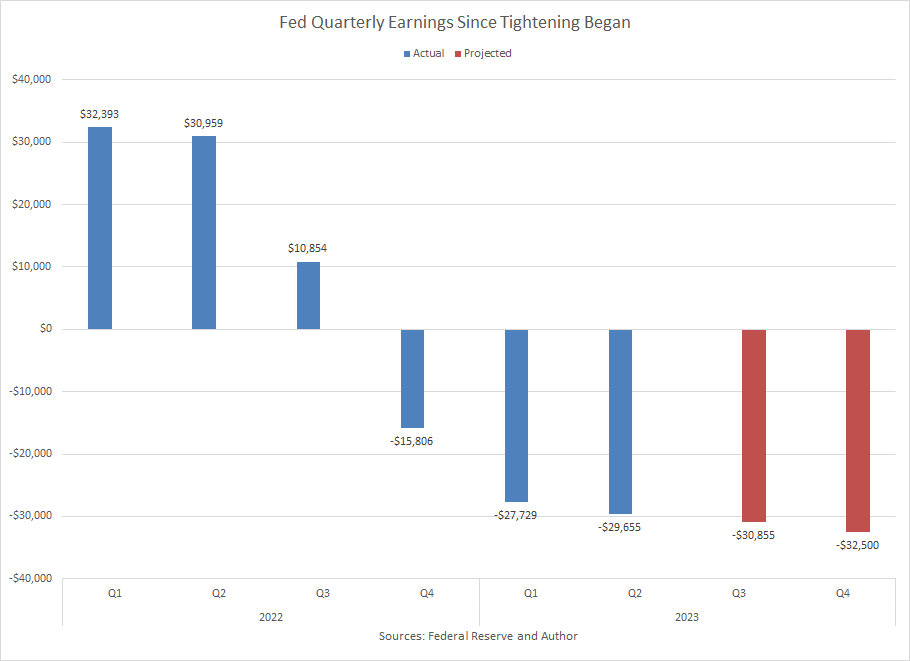

The Fed is currently losing USD 2.5 billion per week…

The impact of the Fed’s rate hikes on the Fed's quarterly earnings since tightening began is obvious. As the Fed tightened, its net interest margin narrowed. In 4Q22, its net interest margin turned negative, and the Fed started to record losses.

Source: Federal Reserve

Can the Fed sustain the losses?

The Fed remits its net earnings to the US Treasury. When there are losses, remittances to the US Treasury are suspended and a “deferred asset” account is created.

This “deferred asset” avoids impacting the Fed's capital account. In other words, the losses do not reduce the Fed’s capital base. This is quite different from conventional operating companies where losses eat into the capital base. When the capital base is exhausted, we have a default. But not the in the case of the Fed. Is this a classic tale of the “emperor wearing no clothes”?

The deferred asset account was negative 95 billion in Aug 2023 - bigger than the Fed’s capital of USD 42 billion. Technically, the Fed should be in default.

To cover the losses, the Fed creates reserves which are essentially loans from the banks. This is not free money! The Fed must pay interest on these reserves. This creates a cycle of accumulating losses.

What else is burning on the Fed’s Balance Sheet?

The Fed carries bonds that it records at an amortized cost basis on its balance sheet. The market value is stated as a footnote. Due to the Fed raising interest rates, the market value of its bonds has fallen. The Fed regards it as an unrealised loss.

For 2Q23 the Fed’s unrealized loss on its bond holdings reached over USD 1 trillion. It is expected to climb as rates rise.

For full year 2023, the Fed will post a record loss. This means the deferred asset account will continue to grow. When the Fed turns profitable, the deferred asset will be reduced. And only when the deferred account turns positive will remittances to the Treasury resume. Based on the Fed's projections, this will not occur until 2030, at the earliest.

By 2026, the Fed’s deferred asset could reach $300 billion versus its capital of USD 42 billion. Unrealized losses of USD 1.5 trillion or more may even be possible.

What can the Fed do?

The Fed’s role is to maintain price stability for economic growth. As such, the Fed says that its operating losses nor its unrealized losses will impair its ability to conduct monetary policy.

Still, the Fed needs to manage the level of losses. Creating reserves to cover operating losses is inflationary, which is counter to the Fed's goal of price stability.

The Fed can reduce losses by cutting the Fed funds rate. But this will run counter to its goal of fighting inflation.

The Fed can suspend paying interest on bank reserves and reverse repurchase agreements. But banks and fund managers would have no incentive to hold reserves at the Fed. The Fed will lose its open market operations toolkit.

The most practical way for the Fed to stop its bleeding is to address the root cause of asset/liability mismatch on its balance sheet. In a way, the Fed is trying to do this through its “Quantitative Tightening” policy – winding down its bond portfolios. This will take time.

While the Fed seemingly minimises the significance of its coming escalating losses, it notably avoids discussion of the losses.

The USA has fiscal problems too…

On the fiscal or government budget side of the house, there is a burgeoning budget deficit. Ultimately, USA taxpayers will pay the bill.

Does the Fed’s Rising Losses Matter?

Many analysts argue that the Fed’s losses are just on paper as the Fed will hold its bonds to maturity.

This may be true, but not if the losses are so large that confidence and trust in the system is eroded. Only because of the USA’s hold on US dollar dominance in international trade, especially in oil and gold, and mainly because of its military power, can this surreal monetary and fiscal anomaly continue. If not, the data points to a “banana currency” situation where the USD will be shunned.

De-Dollarization trend is clear…

In Aug 2023, China's currency regulators apparently asked its banks to reduce or postpone USD purchases. Rather than an affront to the USA, it seemed more likely a goal of slowing the Chinese Yuan’s depreciation.

However, the “de-dollarization” trend is clear. More and more countries are calling for trade to be carried out in other currencies besides the USD. Geopolitical risks and economic dynamics have accelerated the trend to move away from the USD.

It’s not the Fed’s dilemma, but the rest of the world’s…

As it stands, the USA will see more debt ceiling and government shutdown dramas. The USA elections are here again, and the results will cause ripples in the already murky waters.

For now, the Fed will continue its Quantitative Tightening to address its asset/liability mismatch while tuning its Fed funds rate to keep a lid on inflation. Everyone holding the US dollar should watch closely, whether taxpayer or foreign investor.

Stay globally diversified.

Yours sincerely

Victor Lye, BBM CFA CFP®

Founder & CEO

SqSave Investment Team

Disclaimer

The contents herein are intended for informational purposes only and do not constitute an offer to sell or the solicitation of any offer to buy or sell any securities to any person in any jurisdiction. No reliance should be placed on the information or opinions herein or accuracy or completeness, for any purpose whatsoever. No representation, warranty or undertaking, express or implied, is given as to the information or opinions herein or accuracy or completeness, and no liability is accepted as to the foregoing. Past performance is not necessarily indicative of future results. All investments carry risk and all investment decisions of an individual remain the responsibility of that individual. All investors are advised to fully understand all risks associated with any kind of investing they choose to do. Hypothetical or simulated performance is not indicative of future results. Unless specifically noted otherwise, all return examples provided in our websites and publications are based on hypothetical or simulated investing. We make no representations or warranties that any investor will, or is likely to, achieve profits similar to those shown, because hypothetical or simulated performance is not necessarily indicative of future results.

More Articles more

What’s inside SqSave ONE Dollar Portfolios

Team SqSave

Thanks to our proprietary SqSave investment engine, we have automated investing the way it should be - seeking out better returns based on your preferred risk appetite over the medium to long term.

Read more

Decoding Investment Performance: Total Return vs. Time-Weighted Return

Team SqSave

Investing in financial markets comes with its fair share of challenges and complexities.

Read more

SQSAVE PORTFOLIOS DELIVERS RESPECTABLE PERFORMANCE AGAINST COMPETITORS IN 2023

Team SqSave

On a Year-to-Date basis (till end July 2023), all our SqSave reference portfolios outperformed key competitors.

Read more