SqSave Portfolios Performed Strongly in January

15 Feb 2023

Market outlook on the inflation

Last year, many central banks around the world focused on fighting inflation by implementing rate hikes while guiding investors and the general public about the expected economic impact of their rate hiking campaigns (in their attempts to anchor and gradually reduce future inflation expectations). While some global supply chain disruptions are in still in the process of being resolved, inflation in the US is not yet on a clear track to return to the Federal Reserve Bank’s (Fed) long run target level of around 2%. The US labour market and wage inflation outlook will play a crucial role in the next phase of overall progress in the fight against inflation. The tight US job market may keep wage pressures high, which could result in overall inflation remaining persistently higher for longer than markets expect. Consequently, this would extend the current market expected period for when the Fed would feel content enough to start reducing the target Federal Funds Rate again.

The US Fed's recent mixed messaging, however, appears to be suggesting to markets that it may be stumbling towards the next phase of reduced inflation expectations sooner than is reasonable and may signal a near term pause in the Fed's rate hikes. Meanwhile, other major central banks are sending signals contrary to the US Fed, with the European Central Bank (ECB) and Bank of England BOE raising rates last week. This reinforces the view that central banks globally are unlikely to cut rates in unison as soon as markets currently expect. If proven to be true, this could pose added risks on the horizon if markets need to reset their central bank rate reduction expectations.

U.S. stocks rose and Treasury bond yields reversed their drop after the Fed’s most recent FOMC meeting. However, January CPI data showed that inflation is mildly higher than expected, suggesting that while inflation may have peaked, there may still be some way to go before it moderates to normal levels. Hence, the key to the near-term market outlook is whether inflation is shown to remain on track to fall back sufficiently enough to allow the Fed to pause its rates hikes around the current consensus expected terminal rate level; or whether added rate hikes are needed, and what this implies for the chances of an eventual US recession later this year. The U.S. jobs data indicates the Fed has more work to do, while the market is still pricing in rate cuts later in 2023.

SqSave portfolios showing good results

We have benefited from the recovery in the Technology sector, which accounted for relatively larger exposure in the higher-risk portfolios. We have since adjusted our algorithms after a review of the available Exchange Traded Funds and further quantitative optimization. We will be monitoring the February performance closely.

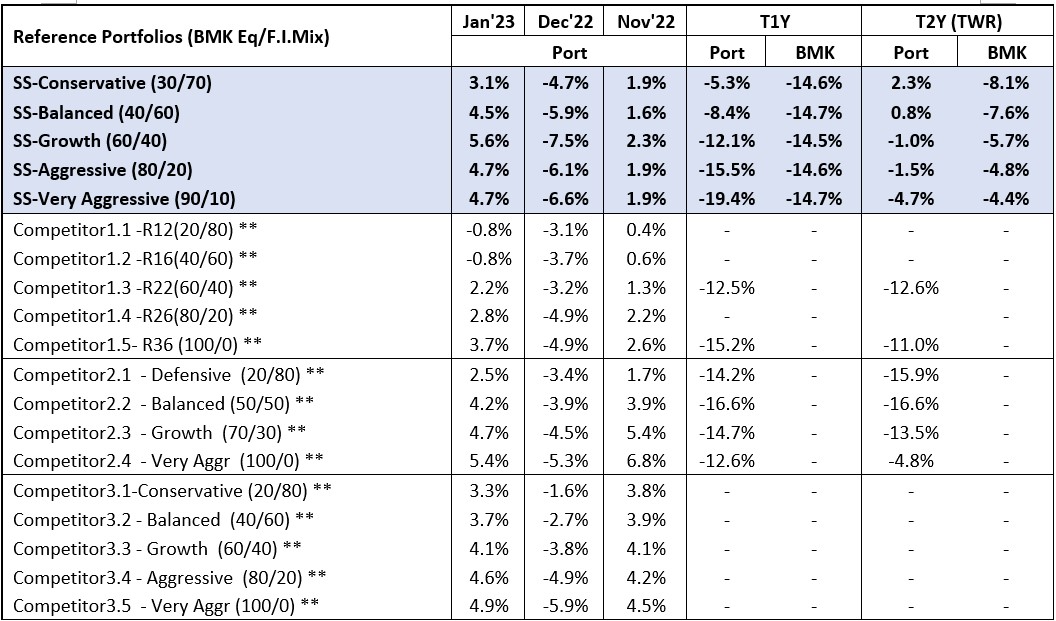

SqSave Reference Portfolios Returns (SGD terms as at 31 Jan 2023)*

*Inclusive of ETF expense ratios and net of SqSave management fees. SqSave uses AI to design and manage diversified investment portfolios for each investor. Because SqSave is not an investment fund, there is no single return measure. Instead, every SqSave investor has his/her own investment performance as each investor is managed separately by our SqSave AI. As investors can withdraw and top-up any time, investment returns will be affected by individual investor decisions. Hence, SqSave uses reference portfolios which are actual portfolios managed on an ongoing basis, without any interference with withdrawals or top-ups, to measure investment performance. ** Performance numbers for competitors are estimates. Abbreviations: BMK: Benchmark; Ret: Return.

Some added noteworthy takeaways from the above performance updates are highlighted below:

- Over the latest trailing 2Y period, all our portfolios have outperformed their competitors, based on available data.

- Over the latest trailing 1Y period, our Low-to-Mid risk portfolios have outperformed their respective benchmarks as well as their competitors (based on available data).

- Our reference Conservative risk portfolio, as of the latest trailing 1Y period, is managing the downside well at -5.3%, while Competitor2 delivered a -14.2% T1Y return.

- In January 2023, all our reference portfolios outperformed comparable competitors’ portfolios, except our Very Aggressive portfolio, which slightly underperformed Competitor2 and Competitor3. We believe that greater weight should be given to long-term performance rather than short-term return differences, which tend to fluctuate on a monthly basis.

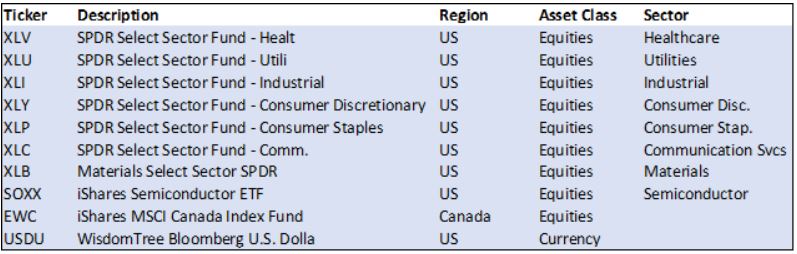

Update on the SqSave ETF Universe

We have broadened our SqSave ETF Universe to enhance the flexibility of our SqSave AI, enabling it to choose from a wider array of potential opportunities for its global investments and to manage market fluctuations through diversification, thereby enhancing potential risk adjusted returns.

We have made some changes to the underlying ETFs in the portfolios. Key changes comprise:

- Included key US-sector ETFs

- Included Canada ETF

- Replaced UUP with USDU (USD bullish fund)

The full list of new ETFs added to our universe for our AI algorithm to select from comprise the following:

In the near future, we expect volatility to generally decrease as it has historically shown a mean-reverting tendency over the long term, especially following prevailing more heightened periods of volatility and adverse market conditions, as was seen throughout 2022. We are confident that our updated ETF Universe should enable our proven AI-driven engine to better manage your investments through added diversification benefits over the long term.

Yours sincerely

SqSave Investment Team

Disclaimer

The contents herein are intended for informational purposes only and do not constitute an offer to sell or the solicitation of any offer to buy or sell any securities to any person in any jurisdiction. No reliance should be placed on the information or opinions herein or accuracy or completeness, for any purpose whatsoever. No representation, warranty or undertaking, express or implied, is given as to the information or opinions herein or accuracy or completeness, and no liability is accepted as to the foregoing. Past performance is not necessarily indicative of future results. All investments carry risk and all investment decisions of an individual remain the responsibility of that individual. All investors are advised to fully understand all risks associated with any kind of investing they choose to do. Hypothetical or simulated performance is not indicative of future results. Unless specifically noted otherwise, all return examples provided in our websites and publications are based on hypothetical or simulated investing. We make no representations or warranties that any investor will, or is likely to, achieve profits similar to those shown, because hypothetical or simulated performance is not necessarily indicative of future results.

More Articles more

ADOPT A CALM AND DISCIPLINED INVESTING APPROACH

Team SqSave

It’s funny to see human psychology confused about investing and gambling.

Read more

Majority of SqSave’s Portfolios Outperformed Peers over Past 2-Years!

Team SqSave

As we approach the end of calendar 2022, we highlight how our SqSave algorithms have managed the lower risk portfolios under heightened market volatility.

Read more

2023 MARKET OUTLOOK

Team SqSave

We are dealing with extended anxiety in recent months. So far this year, the S&P 500 was down over 25% percent at its lowest closing level on 12 Oct 2022.

Read more